Parent Plus Loan Overview

Should you get a Parent Plus Loan, or a Private Student Loan? Read more Below

Introduction

Navigating the financial landscape to support your child’s education can be a daunting task. For many parents, the Parent PLUS Loan offers an opportunity to bridge the gap between savings, scholarships, and the total cost of attendance. As a federal loan designed specifically for parents, it has its own set of advantages and drawbacks. Here, we’ll provide an honest review based on user perspectives to help you make an informed decision.

Pros of Parent PLUS Loans

Availability from the Federal Government

The Parent PLUS Loan is issued by the federal government, which brings a layer of trust and stability. Unlike private loans, you don't have to worry about sudden changes in interest rates or terms that could affect your financial planning.

General Availability Requirements

One of the standout features of the Parent PLUS Loan is its relatively lenient eligibility criteria. This can make it easier for more parents to qualify compared to stringent private loan standards. However, it's important to note that a credit check is still required, and adverse credit history can impact your eligibility.

Eligibility for a Parent PLUS Loan primarily hinges on two fundamental criteria: the applicant must be the biological, adoptive, or, in some cases, the stepparent of a dependent undergraduate student enrolled at least half-time in an eligible school. Furthermore, the applicant must meet the credit requirements, which generally involve not having an adverse credit history. While this may seem daunting, it's important to remember that options such as obtaining an endorser or documenting extenuating circumstances can often provide pathways to approval. Ultimately, these loans aim to support families in their financial journey, ensuring that the dream of higher education remains within reach for their children.

Covers Up to the Cost of Attendance

Parent PLUS Loans can cover up to the total cost of attendance (minus any other financial aid received). This comprehensive coverage can be a lifeline for families facing substantial educational expenses.

Cons of Parent PLUS Loans

Limited Repayment Options

While the federal government offers several repayment plans, the options are limited to:

Standard Repayment Plan

Graduated Repayment Plan

Extended Repayment Plan

These plans may not provide the flexibility needed for parents who face variable financial situations. Moreover, forgiveness options are limited and generally require loan consolidation, which may not always be beneficial.

Higher Interest Rates

Parent PLUS Loans often come with higher interest rates compared to other federal student loans. This can lead to significant long-term costs, especially if you are unable to pay off the loan quickly.

Rates are set to raise to 9.083% for the SY 2024-2025 School Year.

As such, a student with a high quality co-signer might be able to obtain a private student loan for significantly less.

No Income Consideration

Unlike some loan programs that assess your ability to repay based on income, Parent PLUS Loans do not consider your income level.

This might sound like a good deal, but the parent is still on the hook for the payments on these loans. This can lead to significant financial stress on families while their children are in college.

Non-transferable Responsibility

It’s crucial to understand that the Parent PLUS Loan is the parent’s responsibility, not the student’s. This can lead to misunderstandings and financial strain if parents assume the loan will eventually transfer to their child.

Conclusion

The Parent PLUS Loan can be a valuable tool for covering educational expenses, but it requires careful consideration. By understanding both its benefits and limitations, you can better navigate the complexities of funding your child’s education.

If you’re considering a Parent PLUS Loan, I strongly recommend weighing your options, discussing the implications with your child, and perhaps consulting a financial advisor to ensure this is the best path for your family. Taking these steps can help you manage the financial burden more effectively and achieve your educational goals with greater peace of mind.

7.95% Fixed Interest Rate

8.34% to 8.87% APR*

*Rates vary based on number of months to graduation at funding date, NOT your credit score.

Updated July 2nd, 2023

What Students are Saying

"A.M. Money helped me feel understood and taken care of throughout the process. Thanks to A.M., I can now put my mind at ease. I’m less stressed about the demanding financial burden and more focused on my goals.”

Alex | DePaul University

Class of ‘21

“A.M. was very helpful and went above and beyond to make sure that my school and I were informed through the process.”

Kalund | North Carolina State

Class of ‘20

“A.M. is fair and the most competitive company I've come across, so you can feel confident in managing your money and your education. Seriously, dump Discover. A.M. Money made working toward my college degree possible.”

Brii | DePaul University

Class of ‘21

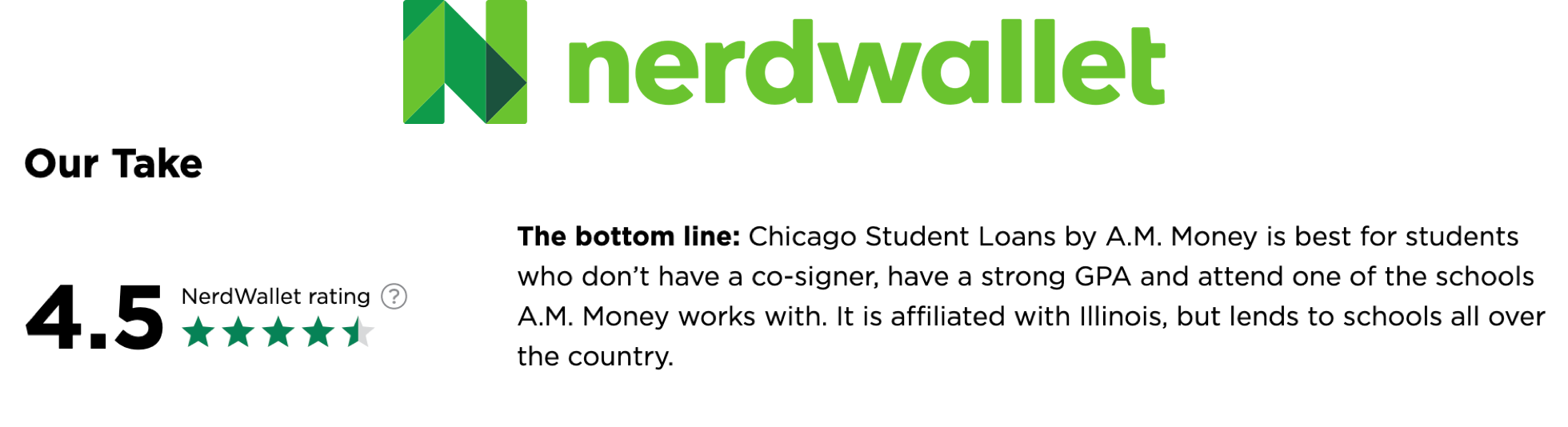

What Experts are Saying

As Seen on